September 22, 2014

The most exciting event of last week was undoubtedly the listing of Chinese e-commerce giant, Alibaba Group Holding, on the New York Stock Exchange. The Alibaba share listed at $92.70, a whopping 36 per cent premium to the offer price, proving right analysts who felt that the IPO price was conservative.

September 22, 2014

The most exciting event of last week was undoubtedly the listing of Chinese e-commerce giant, Alibaba Group Holding, on the New York Stock Exchange. The Alibaba share listed at $92.70, a whopping 36 per cent premium to the offer price, proving right analysts who felt that the IPO price was conservative.

The scale of Alibaba’s listing success should be evident from the following: the $21.8 billion it raised (could get close to $25 billion if the issue managers decide to accept the excess subscriptions) was the highest amount ever raised by an internet company in the U.S. It was much larger than Facebook’s $16 billion and Twitter’s $2 billion.

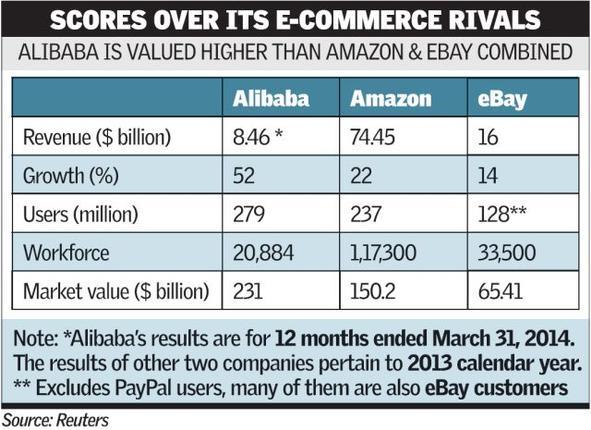

The valuation of $231 billion that it secured on listing day now makes it the 11 most valuable listed company in the U.S. ahead of the bluest of blue chips such as Procter & Gamble, Pfizer, IBM and Coca Cola.

Jack Ma, who founded Alibaba with $60,000 in an apartment at Hangzhou, south-west of Shanghai, in 1999, is now the richest man in China with a net worth of close to $22 billion.

The 49-year old former school teacher has not only inspired a thriving start-up culture in China but has also created immense wealth for employees, a number of whom are vested with shares in the company.

Jack Ma, China's richest man

Scene in India

In the backdrop of Alibaba’s success, it is tempting to look at the scene in India. Admittedly, there is no comparison between China and India when you consider key numbers such as internet penetration, on-line buyers and e-commerce sales volumes.

Compared to China’s estimated $180 billion e-commerce market, India’s is a piffling $13 billion, according to a study by KPMG and Internet and Mobile Association of India. About 70 per cent of India’s market comes from online travel transactions.

India’s internet users number a little over 200 million: China has more than thrice that at 632 million and is projected to touch 850 million by 2015. India is projected to cross the 500-million mark by 2018. The number of on-line buyers in India is expected to cross the 39-million mark by end of this year; in contrast, Alibaba alone has 279 million active buyers in China!

There are two ways of looking at these numbers. The first is to fret over how far ahead China’s e-commerce market is and how Indian consumers are still in the brick-and-mortar shopping era. The other, more optimistic way, of looking at the comparative data is to realise the potential that India holds for growth in the e-commerce space. That is exactly the attitude and approach of those such as Flipkart, Jabong, Snapdeal, eBay and Amazon in India.

The optimism seems to have rubbed off on financiers as well — Flipkart bagged $1 billion in funding in July which valued the company at $7 billion. In barely three months since the previous funding round in May, Flipkart’s valuation had more than doubled prompting founder Sachin Bansal to dream of turning into a $100-billion company in the next five years.

Not just Flipkart, its much larger rival, Amazon, has also been stepping on the accelerator in India. Within a day of Flipkart announcing its $1 billion funding, the U.S. e-commerce giant said it would be investing $2 billion in India. Why this burst of optimism in the industry?

For one, the number of on-line buyers is projected to treble to 128 million by 2018 according to research firm Forrester. If the growth in mobile penetration is any indication, this is a conservative projection given that half of all internet users in India are based on mobile platforms. The competition is to grab as much of the new users as possible.

Yet, where the players could be going wrong in India is on their revenue-first strategy unmindful of profitability. While the likes of Amazon and eBay may have deep pockets, the same cannot be said about their domestic counterparts, the large funding rounds notwithstanding.

Alibaba was smart in its business strategy which ensured that it would be profitable. For instance, with millions of products vying for customer attention on its portal, Alibaba devised options for sellers to advertise on its site and also set up attractive online storefronts for a fee.

It also leveraged on its massive size in terms of registered customers by blocking search engines such as Baidu from trawling its e-commerce portals when users search for shopping options. Perforce, Alibaba forced buyers to approach it directly and thus made its portals attractive for advertisers. Alibaba thus captured the advertisement revenue that would have gone to Baidu otherwise.

While it is understandable that the Flipkarts and the Jabongs may be eyeing Alibaba’s success longingly the fact is that they need to devise similar innovative strategies to turn profitable. Flipkart already boasts of 27 million registered buyers — two-thirds of total online buyers in the country — which can be leveraged to attract advertisers in a bigger way. The Indian e-commerce industry is obviously beginning to take-off.

It will be interesting to watch whether it will eventually spawn a local Alibaba or will it be consumed by giants such as Amazon or eBay. Or who knows, even Alibaba.

Courtesy: PTI

{kind=link}