September 11, 2013

BEIJING/LONDON: Long after concerns about tightening US monetary policy have faded, a more profound issue will still dog global policymakers: how to handle the second stage of China's economic revolution.

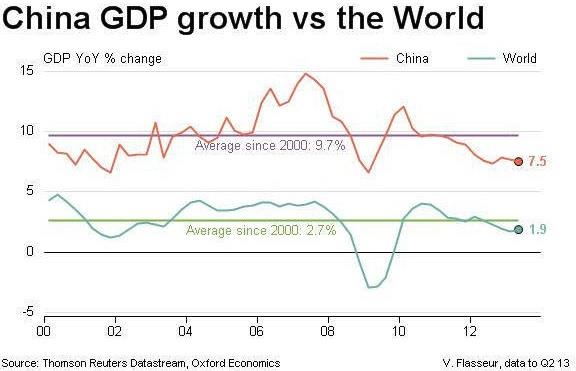

China will remain the most powerful engine of global growth for the next couple of decades.

September 11, 2013

BEIJING/LONDON: Long after concerns about tightening US monetary policy have faded, a more profound issue will still dog global policymakers: how to handle the second stage of China's economic revolution.

China will remain the most powerful engine of global growth for the next couple of decades.

The first phase, industrialization, shook the world. Commodity-producing countries boomed as they fed China's endless appetite for natural resources. Six of the 10 fastest-growing economies last decade were in Africa.

China's flood of keenly priced manufactured goods hollowed out jobs in advanced and emerging nations alike but also helped cap inflation and made an array of consumer goods affordable for tens of millions of people for the first time.

The second stage of China's development promises to be no less momentous.

Consumption will take over the growth baton from investment. Services will grow as a share of the economy, while industry shrinks. Commodity-intensive mass manufacturing based on cheap labour will give way to greener, cleaner ways of making things.

More of the value added by a better-educated, more productive workforce harnessing new technologies will stay in China instead of going to multinational companies.

That's the plan, anyway.

China will remain the most powerful engine of global growth for the next couple of decades, but it will no longer be just processing imported raw materials and components for re-export, said Li Jian with the Chinese Academy of International Trade and Economic Cooperation, the Commerce Ministry's think tank.

"China has realized that it cannot blindly rely on investment and exports as the main drivers of growth. So China's demand will be more balanced," Li said.

High stakes

To show it is serious about more sustainable growth, China deliberately engineered the first-half slowdown that unnerved markets in order to address these longer-term structural priorities, according to President Xi Jinping.

Xi and the other new leaders of China's Communist Party are expected to approve a blueprint for reform at a plenum in November. Overcoming vested interests opposed to the new economic model will be a stern test of their credibility.

A lot is at stake for the global economy too.

Philip Schellekens, an economist with the World Bank in Washington, said the importance of the reforms Beijing intends to make cannot be overstated. As China changes, so will the rest of the world.

"The structural transformations that we think are going to happen in China over the next two decades will matter far more than the near-term vulnerabilities," he said.

On balance, commodity-exporting developing economies stand to be affected more than rich nations – an obvious exception being Australia, where the end of a China-driven mining boom was a big issue in Saturday's election. China buys a third of Australia's exports.

Commodity demand should stay strong, especially as China's capital stock per head is only 10 percent that of America's and urbanization has a long way to go. But rebalancing will favor commodities more closely tied to consumption than to investment.

Economists fret that too many emerging markets spent their windfalls from surging raw material prices instead of ploughing them into infrastructure and other investment. As a result, growth is slowing now that China's demand is softening.

China's appetite for agricultural commodities and energy should hold up well but Capital Economics, a London consultancy, said it was concerned about large metals exporters that have not saved their extra income and so are running current account deficits.

It singled out South Africa, Zambia, Chile and Peru as being particularly vulnerable.

Winners and losers

Of course, lower raw material prices should boost growth and lower inflation for commodity importers.

Take iron ore. With no other country coming close to being able to absorb the slack left by China, which imports about two-thirds of the world's ore, prices risk years of decline as a major oversupply swamps demand, with some forecasting prices to be cut in half by 2015.

Another bonus is that big emerging markets such as India and Indonesia will have a chance to move into basic manufacturing sectors that China is vacating. Bangladesh has quickly become the world's second-biggest textile exporter.

Brazil stands out as an example of a country that has already been under intense pressure from China in low-skill industries such as footwear and will increasingly be going head to head with China in higher-value markets too. Policies to boost competitiveness thus become more imperative than ever.

After largely missing the chance to reform during the boom, Brazil also risks squandering the opportunities thrown up by China's transition slip unless it improves its infrastructure, cuts red tape and overhauls its tax system, economists say.

"Some of the underlying structural shortcomings of the economy were covered up during the bonanza. It's only as the commodity boom has slowed that the supply side constraints have become more visible," said Jens Arnold, who tracks Brazil for the Organization for Economic Cooperation and Development in Paris.

In the case of advanced economies, China's transition is a double-edged sword, according to He Yifeng, an analyst at Hongyuan Securities in Beijing.

"For the United States and Europe, China's rebalancing could create more competition for them. But they can take the initiative by focusing on the higher end of the value chain, relying on knowledge and technology exports," he said.

Services bonanza

Already a lucrative market for European purveyors of luxury goods, China will increasingly present opportunities for foreign firms as incomes rise and consumers grow more discriminating.

Safety-conscious parents' choice of foreign-made baby milk formula is a case in point, said Haibin Zhu, chief China economist for JP Morgan in Hong Kong.

"We will probably see a shift in the consumption basket," Zhu said. "The increased focus on product quality is positive news for many international exporters, particularly from advanced economies."

Another rich seam for advanced economies is services, which account for just 43 percent of Chinese GDP, the smallest share of any major economy.

James Emmett, global head of trade finance at HSBC in London, said urbanisation and the rise of China's middle class offered openings to firms in Britain and beyond in sectors such as health, education and tourism.

"We are seeing a change in the nature of China," he said.

As services blossom, foreign companies could reap a windfall of up to $6 trillion by 2025 in everything from retail trade and transport to hotels and finance, said Yale University's Stephen Roach, a former chairman of Morgan Stanley Asia.

Zhu at JP Morgan expects investment to drop from 48 percent of GDP to 35 percent by 2018-2020 as consumption (household and government) rises to 60-65 percent from 50 percent.

At the same time, GDP growth is likely to slow toward 6.5 percent a year by 2016-2020 from 7.7 percent in 2012 and 10 percent a year on average since the late 1970s.

Yet market worries about the transition need to be kept in perspective. Even if growth slows to 5 percent a year by 2030, Schellekens with the World Bank said China will still be adding output every year equal to the size of the South Korean economy.

"Even though China is facing quite a transformation, the long-term future is still a very positive one," he said.

Courtesy: Reuters

{kind=link}