JANUARY 26, 2022

Los Angeles Rams wide receiver Odell Beckham Jr. is among the professional athletes who have struck promotional deals that involve converting their salaries into crypto. (Photo by Kevin C. Cox/Getty Images)

By the end of last year, the value of Hasten Carter’s cryptocurrency holdings had climbed to about $250,000. He moved to a nicer apartment, bought a new truck, and started thinking about pursuing his dream of a full-time career in game development.

But over the past two months, the value of cryptocurrencies has plummeted, taking with it much of Carter’s digital nest egg, a mix of Ethereum, the second-most popular cryptocurrency, and a number of more obscure coins.

“It’s gotten out of hand to the point where I’m not sure I’m comfortable I can keep my money,” said Carter, 30, who has kept his day job at a Nashville sign-making business. Of his hopes for a new career, he said: “I’m not sure if it’s as wise of a decision.”

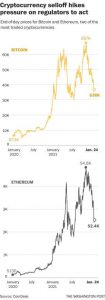

Thousands of Americans who jumped into crypto investing over the past two years in hopes of a rocket ride to instant wealth now face a similar reckoning: Prices for cryptocurrencies — from relative stalwarts such as bitcoin and Ethereum to more exotic tokens — have cratered since reaching all-time highs in early November, wiping out an astonishing $1.35 trillion in value globally, nearly half of the total market, according to CoinMarketCap.

The slide has accelerated over the past week as investors have fled riskier bets for safer harbors. The “crypto crash” has put pressure on Washington regulators to impose stricter rules on the industry — and raised fresh questions about the dangers of cryptocurrency for the average investor.

“You’re going to get more people calling their elected representatives, generally unhappy about crypto or feeling they were wronged in some way,” said Ian Katz, managing director of Capital Alpha Partners, a Washington policy analysis firm. “All regulators and members of Congress want to appear to be alert behind the wheel, and if this turns out to be a continued bloodbath, it increases the impetus for action.”

The plunge in crypto prices has tracked a stock market sell-off that has seen the broad-based S&P 500 shed about 8 percent of its value this year, as investors brace for interest rate hikes from the Federal Reserve and potentially underwhelming corporate earnings.

Yet both the crypto and stock markets are attempting to claw back some of their recent losses. Bitcoin, which was trading below $33,000 on Monday morning, recovered to around $37,000 on Tuesday afternoon. And after two days of wild swings, the S&P 500 and the Dow Jones industrial average stood at their levels at the start of the week.

In the meantime, the crypto swoon is hitting celebrities and everyday investors alike. A number of star athletes have entered into promotional deals with crypto companies that involve converting at least part of their salaries into digital assets. Los Angeles Rams wide receiver Odell Beckham Jr. announced in late November he would be converting $750,000 of his 2021 pay into bitcoin as part of an agreement with the payment service Cash App.

If Beckham converted that amount in a lump sum at the time, it could be worth as little as $35,000 now, after factoring in bitcoin’s slide and his tax burden on the original payment, according to Action Network analyst Darren Rovell.

The industry’s surge has drawn in a widening circle of Americans: One in 6 now say they have invested in, traded or otherwise used cryptocurrency, according to a recent Pew Research Center study. And that pool is increasingly diverse. Forty-four percent of those who have bought or traded crypto in the past year are non-White, and 35 percent have annual household incomes below $60,000, according to a poll over the summer by NORC at the University of Chicago.

Many crypto holders remain undeterred. Relative veterans point to their experience holding on through a crash in prices in late 2017 and early 2018 that investors now call the “crypto winter” — and the dramatic rally that followed it. They say recent price fluctuations have not shaken their faith in the technology’s long-term value, bidding farewell to new investors with a kind of “so long, leaves more for the rest of us” élan.

“Goodbye to all the nonbelievers,” David Hoffman, co-owner of Bankless, tweeted on Saturday, as prices continued to plummet.

In an interview with The Post, Hoffman, whose company hosts a newsletter, podcast and Discord group about crypto, said his circle of friends, which formed during the crash four years ago, almost feel more comfortable in a down cycle.

“We were all born in the bear market, so finally we’re back home,” he said, noting Ethereum is now worth $2,400, “and last time it was $80.”

“Obviously no one is happy to see their portfolio shrink 40 percent in seven days, but it’s really a matter of: Do you believe crypto is going to be the dominant financial platform of the future?” Hoffman said.

Likewise, newly wealthy crypto holders who moved to Puerto Rico in the past year to take advantage of tax breaks on crypto investments have not seen much impact from recent price fluctuations, said George Burke, a tax break beneficiary who moved to the island last May.

“The crypto people here are likely long-term holders. Many, like me, have been in the space for years and seen multiple price cycles. No need for any of us to panic sell. We’ve seen it before,” said Burke, co-founder and chief marketing officer of Portal, a peer-to-peer cryptocurrency trading platform incorporated in Delaware.

Portal did consider the market moves in deciding whether to go forward with its planned public sale, since “public sentiment and investor contributions” are closely tied to the price of bitcoin, said Burke, whose company has four team members based on the island. Ultimately, they decided to move forward.

“I personally think this slump is very temporary,” he said.

Nonetheless, the crash is resonating in Washington, where White House officials are working to better coordinate what has been a fractured approach to crypto from federal agencies haggling over how to regulate the new asset class.

White House officials plan to release as soon as this month a memorandum that people familiar with the matter said would span numerous topics related to cryptocurrencies. Those include White House guidance surrounding a central bank digital currency, a form of digital cash that would be backed by the Federal Reserve and could compete with some privately issued cryptocurrencies. The White House is also expected to weigh in on the impact of crypto on the stability of financial markets and the need to sync regulations of digital currencies with other countries that may have different approaches.

The White House effort — ongoing since last summer but first made public in a Bloomberg News report — is not expected to contain significant policy recommendations. But it is likely to designate further action to parts of the federal government, including the Treasury Department and the Securities and Exchange Commission. The White House memorandum is expected to be produced by the National Security Council.

“The White House wants to send the clear message it is fostering a coordinated approach related to cryptocurrencies rather than a scattershot approach from the regulatory agencies,” one person familiar with the matter said, speaking on the condition of anonymity to discuss an administration matter not yet made public. “They’re going to use the document to set up a framework for different agencies to start working on different assets important to both financial stability and national security.”

But regulators focused on the industry aren’t waiting to press ahead. Securities and Exchange Commission Chairman Gary Gensler, arguably the administration’s most aggressive advocate for tougher oversight, last week said his agency is eyeing new rules for crypto trading platforms. Without them in place, “it’d be another year of the public being vulnerable,” he said in a virtual roundtable with reporters.

The SEC has taken 97 enforcement actions against industry players since 2013, including 24 last year, according to Cornerstone Research.

Jose Santana Torres, a taxi driver who began trading cryptocurrency around 2018, after accepting payment for rides in bitcoin, said he felt insulated from volatile market shifts because he moved valuable holdings in bitcoin and Ether into Tether, a “stablecoin” that claimed to be backed by an equivalent amount of U.S. dollars. The company was ordered to pay a $41 million fine to the U.S. Commodity Futures Trading Commission in October to settle allegations that the claim was misleading.

“Still holding it for the next bull run. … Not a big deal for me,” he said.

Courtesy/Source: Washington Post

{kind=link}