DECEMBER 26, 2019

Dan Herron, CPA, at the New York City Marathon in 2013

Dan Herron, CPA, didn’t want to be the bearer of bad news, yet there he was explaining to a couple why they owed the federal government approximately $10,000 in taxes on their 2018 return.

“They were used to paying around $1,100,” the San Luis Obispo, Calif., accountant said.

The couple had three children, all under the age of 6, and were homeowners in southern California. “They were hit with this huge tax bill,” said Herron, principal of Elemental Wealth Advisors.

They could attribute it to the Tax Cuts and Jobs Act, the first major overhaul of the tax code in more than 30 years.

President Donald Trump, who signed the bill into law at the end of 2017, championed the measure and reportedly wanted to dub it the “Cut Cut Cut Act.”

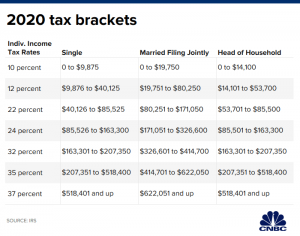

Indeed, the new law cut taxes across the board. It trimmed individual income tax rates, bringing the top rate down to 37% from 39.6%. Corporations also got relief, as their income tax rates fell to 21% from 35%.

The federal law also raised the standard deduction for single filers to $12,000 in 2018 from $6,350 for in 2017 (it went to $24,000 from $12,700 for married-filing-jointly) and limited certain itemized deductions for taxpayers.

It also did away with personal exemptions: a $4,050 deduction you once could claim for yourself and each dependent in your household.

The kicker is that many of these provisions are temporary, so they will expire at the end of 2025.

The Tax Cuts and Jobs Act made what was an abstract concept — the Internal Revenue Code — into hotly debated topic that left many Americans wondering whether they really got the tax cut they were promised.

“We spent a lot of time explaining to people how their taxes were reduced in the prior year, but they still owed more on April 15,” said Edward J. Reitmeyer, CPA and regional partner-in-charge at Marcum LLP.

“When you couple that confusion with the political environment where everyone was on edge, it added fuel to the fire,” he said.

Withholding changes

In early 2018, the IRS and Treasury Department released its new withholding tables to reflect the tax overhaul.

The tables are intended to work with a key form, known as a W-4, that determines the amount of income tax withheld from your pay, based on whether your spouse works and the number of dependents you have at home.

Having a correct W-4 on file can make the difference between owing the IRS come tax season because you’ve withheld too little tax — or getting a hefty refund because you overpaid the taxman during the year.

Here’s where many Americans got tangled up as the new tax law lowered rates across the board.

However, if you were already withholding less tax from your pay — either because you had itemized deductions in previous years or you claimed multiple exemptions for your dependents — you likely paid too little in tax during 2018 and wound up owing in April 2019.

This confounded taxpayers, as they measured the success of the new tax law based on whether they had bigger refunds.

Instead, they paid less tax over the year, which meant they kept more of their take-home pay. However, they may have received smaller refunds from Uncle Sam as a result or they may have owed if they paid too little in tax.

The IRS issued 111.6 million refunds for 2018 returns filed through Nov. 22, with taxpayers receiving an average refund of $2,860.

In comparison, the federal agency gave 111.9 million refunds for 2017 returns filed through Nov. 23, 2018, with an average refund of $2,899.

“The biggest way the new tax law was botched was the failure to communicate the difference between a lower tax liability for the year versus lower tax bills in April,” said Jeffrey Levine, CPA and director of financial planning at BluePrint Wealth Alliance.

To that end, you could have pocketed an extra $100 per paycheck over the course of 2018 because of lower taxes. However, if you wound up owing $500 come tax time instead of getting the $1,500 refund you’re accustomed to, it’s unwelcome news.

For Herron, the California accountant, his client’s family of five wound up withholding too little, as they had claimed exemptions for each of the kids and also faced limits on their ability to claim a deduction for state income and property tax.

“They had a lot of exemptions that weren’t adjusted going into 2018, which caused the underwithholding,” Herron said. “This was actually a common thing we saw for people between 2017 and 2018.”

Standard vs. itemized deductions

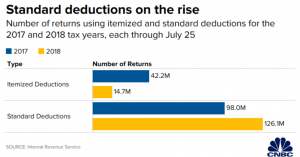

With the standard deduction being nearly doubled, significantly fewer people claimed itemized deductions — which include write-offs for mortgage interest, medical expenses, state and local taxes, and charitable giving.

Consider that prior to the tax overhaul, 42.2 million taxpayers took itemized deductions on their 2017 returns, the IRS found in its analysis of forms submitted through July 25, 2018.

That figure declined after the Tax Cuts and Jobs Act: 14.6 million households claimed itemized deductions on their 2018 returns, according to an IRS analysis of filings submitted through July 25, 2019.

Taxpayers now must weigh whether it makes sense to incur certain expenses if they are less likely to itemize.

For instance, charitable giving by individuals fell to $292 billion in 2018, a 1.1% drop from 2017, according to Giving USA.

The organization attributed some of that decline to the decrease in people who are itemizing on their returns.

“If you’re 65 and married to someone who’s 65, you have to exceed over $27,000 in itemized deductions, and you’ll see no benefit until you get to more than $17,000 in charitable contributions,” said Levine. “Very few people who are retired are doing that.”

Lumping at least two years’ worth of charitable gifts, known as “bunching,” has emerged as a way to help taxpayers itemize in alternating years.

Cutting SALT

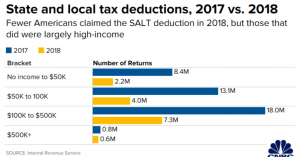

Perhaps the most contentious change to itemized deductions was a new $10,000 limit on the extent to which filers could claim state and local taxes.

These so-called SALT deductions included write-offs for state and local income, property and sales taxes.

“For more people, it became very expensive to live in those high-tax states — not just New York and Connecticut, but any state where you’re charged income tax and you’re paying more than $10,000,” said Tim Steffen, CPA and wealth management consultant with PIMCO.

Indeed, among New Yorkers who itemized in 2017, those who claimed SALT deductions wrote off an average of $23,804, according to the Tax Policy Center.

In Connecticut, the average SALT deduction in 2017 was $20,905, while Californians took an average of $20,451, the center found.

Controversy over the limits has spurred the affected states into litigation against the federal government.

Inability to deduct those high income and property taxes has also made tax-free havens like Florida even more appealing to New Yorkers.

Empire State residents who have relocated to the Sunshine State in 2019 include President Donald Trump and billionaire Carl Icahn.

Overhaul the approach

While taxpayers generally gear up to file by April 15, accountants say the new tax law made planning a year-round affair.

That’s because whether you’re fine-tuning your tax withholding, planning the tax-savviest way to give to charity or weighing a move to an income-tax free state, you’ll want your CPA to draft a projection of your finances before you proceed.

“This is the reason why tax preparation is a dying business, but tax planning is still alive and well,” Levine said.

“Singling out how to avoid penalties and prepare for the tax law at the end of the year is where planning comes in,” he said.

Courtesy/Source: CNBC

{kind=link}