October 19, 2017

The Internal Revenue Service has announced the annual inflation adjustments for a number of tax-related provisions for 2018, including, of course, the latest tax rate schedules and tax tables.

MFJ 2018

October 19, 2017

The Internal Revenue Service has announced the annual inflation adjustments for a number of tax-related provisions for 2018, including, of course, the latest tax rate schedules and tax tables.

MFJ 2018

These are the numbers for the tax year 2018 beginning Jan. 1, 2018 (assuming that there are no big changes as the result of tax reform). They are not the numbers and tables that you’ll use to prepare your 2017 tax returns in 2018 (you’ll find them here). You’ll use these numbers to prepare your 2018 tax returns in 2019.

If you aren’t expecting any significant changes in 2018, you can use the updated tax tables and other tax numbers to estimate your liability. If you expect to make more money or have a chance in your circumstances (i.e., get married, buy a house, start a business, have a baby), consider adjusting your withholding or tweaking your estimated tax payments.

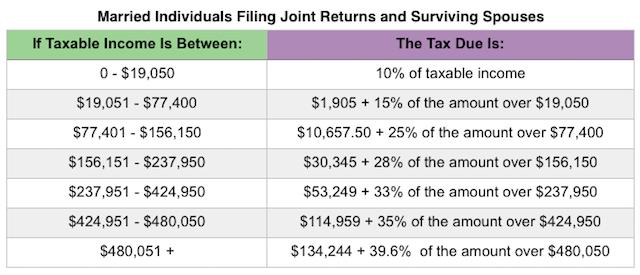

Tax Brackets and Tax Rates. The big news is, of course, the tax brackets and tax rates for 2018. The top tax rate remains 39.6%. The other marginal rates are: 10%, 15%, 25%, 28%, 33% and 35% (there is also a zero rate). Here’s how it breaks out:

You can compare these numbers to the 2017 tables here.

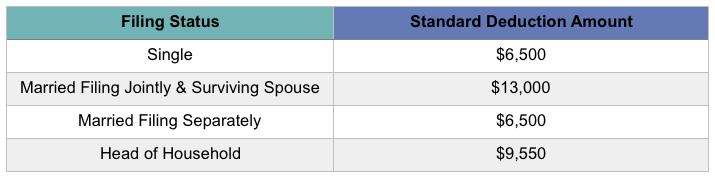

The standard deduction for single taxpayers and married couples filing separately is $6,500 in 2018, up from $6,350 in 2017; for married couples filing jointly, the standard deduction is $13,000, up from $12,700 in the prior year; and for heads of households, the standard deduction is $9,550 for 2018, up from $9,350. The numbers look like this:

Std Deduction

- For 2018, the additional standard deduction amount for the aged or the blind is $1,300. The additional standard deduction amount increases to $1,600 for unmarried taxpayers.

- For 2018, the standard deduction for a taxpayer who can be claimed as a dependent by another taxpayer cannot exceed the greater of (a) $1,050 or (b) $350 plus the dependent’s earned income.

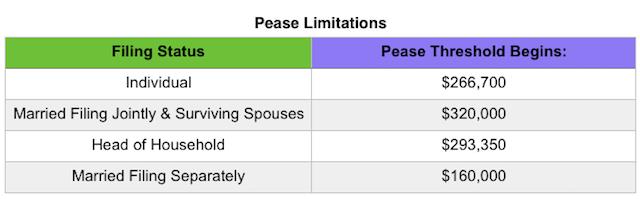

- For high-income taxpayers who itemize their deductions, the Pease limitations, named after former Rep. Don Pease (D-OH) may cap or phase out certain deductions. The Pease thresholds for 2018 are:

Pease Limitations

If the Pease limitations apply, the total of your itemized deductions is reduced by the lesser of 3% of AGI above the threshold or 80% of the amount of itemized deductions otherwise allowable. Pease limitations apply to charitable donations, the home mortgage interest deduction, state & local tax deductions, and miscellaneous itemized deductions. They do not apply to medical expenses, investment expenses, gambling losses, and certain theft & casualty losses.

(You can read more about the Pease limitations and how they affect high-income taxpayers here.)

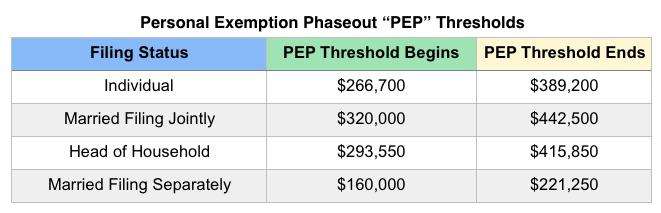

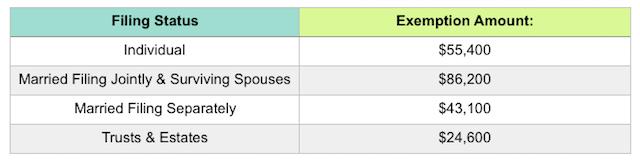

The personal exemption amount for 2018 is $4,150. However, the exemption is subject to a phase-out for married taxpayers with an adjusted gross income (AGI) beginning at $266,700 ($320,000 for married couples filing jointly) and phasing out completely at $389,200 ($442,500 for married couples filing jointly). Other phaseouts apply as follows:

PEP 2018

The alternative minimum tax (AMT) exemption amounts are now permanently adjusted for inflation. For 2018, the AMT exemption amounts are as follows:

AMT 2018

The kiddie tax applies to unearned income for children under the age of 19 and college students under the age of 24. Unearned income is income from sources other than wages and salary, like dividends and interest. For 2018, the kiddie tax threshold – meaning the amount of unearned net income that a child can take home without paying any federal income tax – remains at $1,050. That means all unearned income in excess of $2,100 is taxed at the child’s parent’s tax rate.

There’s an AMT for the kiddie tax, too. For 2018, the AMT exemption amount for the kiddie tax may not exceed the sum of the child’s earned income plus $7,650.

Some tax credits are also adjusted for 2018. Some of the most common tax credits are:

– Earned Income Tax Credit (EITC). For 2018, the maximum EITC amount available is $6,444 for taxpayers filing jointly who have 3 or more qualifying children. The revenue procedure has a table providing maximum credit amounts for other categories, income thresholds, and phase-outs.

– Child & Dependent Care Credit. For 2018, the value used to determine the amount of credit that may be refundable is $3,000 (the credit amount has not changed). Keep in mind that this is the value of the expenses used to determine the credit and not the actual amount of the credit.

– Adoption Credit. For 2018, the credit allowed for an adoption of a child with special needs is $13,840, and the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $13,840. Phaseouts apply beginning with modified adjusted gross income (MAGI) in excess of $207,580 and completely phased out for taxpayers with MAGI of $247,580 or more.

– Hope Scholarship Credit. The Hope Scholarship Credit for 2018 will remain an amount equal to 100% of qualified tuition and related expenses not in excess of $2,000 plus 25% of those expenses in excess of $2,000 but not in excess of $4,000. That means that the maximum Hope Scholarship Credit allowable for 2018 is $2,500.

– Lifetime Learning Credit. As with the Hope Scholarship Credit, income restrictions apply to the Lifetime Learning Credit. For 2018, the adjusted gross income amount used to determine the reduction in the Lifetime Learning Credit is $57,000 (or $114,000 for joint filers).

Changes were also made to certain tax deductions, deferrals & exclusions for 2018. You’ll find some of the most common here:

– Student Loan Interest Deduction. For 2018, the maximum amount that you can take as a deduction for interest paid on student loans remains at $2,500. Phaseouts apply for taxpayers with modified adjusted gross income (MAGI) in excess of $65,000 ($135,000 for joint returns) and is completely phased out for taxpayers with modified adjusted gross income (MAGI) of $80,000 or more ($165,000 or more for joint returns).

– Foreign Earned Income Exclusion. For tax year 2018, the foreign earned income exclusion is $104,100, up from $102,100 for tax year 2017.

– Transportation and Parking Benefits. For 2018, the monthly limitation for the qualified transportation fringe benefit is $260 (up just $5) for transportation in a commuter highway vehicle or any transit pass, as well as qualified parking.

– Medical Savings Accounts (MSA). For 2018, a high deductible health plan (HDHP) is one that, for participants who have self-only coverage in an MSA, has an annual deductible that is not less than $2,300 but not more than $3,450; for self-only coverage, the maximum out of pocket expense amount is $4,500. For 2018, HDHP means, for participants with family coverage, an annual deductible that is not less than $4,600 but not more than $6,850; for family coverage, the maximum out of pocket expense is $8,400.

Taxpayers that don’t maintain health insurance coverage must claim a waiver or exemption or be subject to the shared individual responsibility payment. For 2018, that penalty is equal to 2.5% of your adjusted gross income (AGI), or $695 per adult and $347.50 per child, up to a maximum of $2,085, whichever is higher. That amount is unchanged from 2017.

And remember that passport revocation rule? For 2018, the amount of a serious delinquent tax debt is defined as $51,000 for those purposes.

For federal gift and estate tax rates, check out this post from Forbes’ Ashlea Ebeling. More cost-of-living and other adjustments are available through Rev. Proc. 2017-58 (downloads as a pdf).

Courtesy/Source: Forbes

{kind=link}